At the end of July, the forbearance is scheduled to be lifted. Unless there’s a change in this expiration of protections, many landlords may have trouble paying their mortgages on investment properties. Right now, renters are able to pay dues, but what happens when the economic stimulus runs out and unemployment stops paying an extra $600 per month? Experts predict a downturn in renter’s ability to pay. Unless unemployment rates drastically increase, we’ll be seeing a large increase in foreclosures and homes for sale.

Current projections:

You can read 15 articles from reputable sources on the subject of the impact of coronavirus on the housing market and get 15 different predictions on the upcoming years of recovery to match. This can make it difficult to make a decision on whether to look into investment homes or to wait it out.

You can read 15 articles from reputable sources on the subject of the impact of coronavirus on the housing market and get 15 different predictions on the upcoming years of recovery to match. This can make it difficult to make a decision on whether to look into investment homes or to wait it out.

What we’re finding is there are two basic camps of thought. The first camp is pretty optimistic about purchasing right now. These projections include steadily low interest rates1, more of a “softening” of the market, rather than a crash2, and a work from home increase that will push renters into larger homes. The second camp is more of a “play it safe” option. Those who follow these projections see the housing market up for a wild ride in the next several years due to coronavirus and would stress the importance of the lack of ability to actually predict what will happen in that time. Both arguments are valid and have a place! But does that help you make a decision? No. Probably not.

Option 1: Jump In!

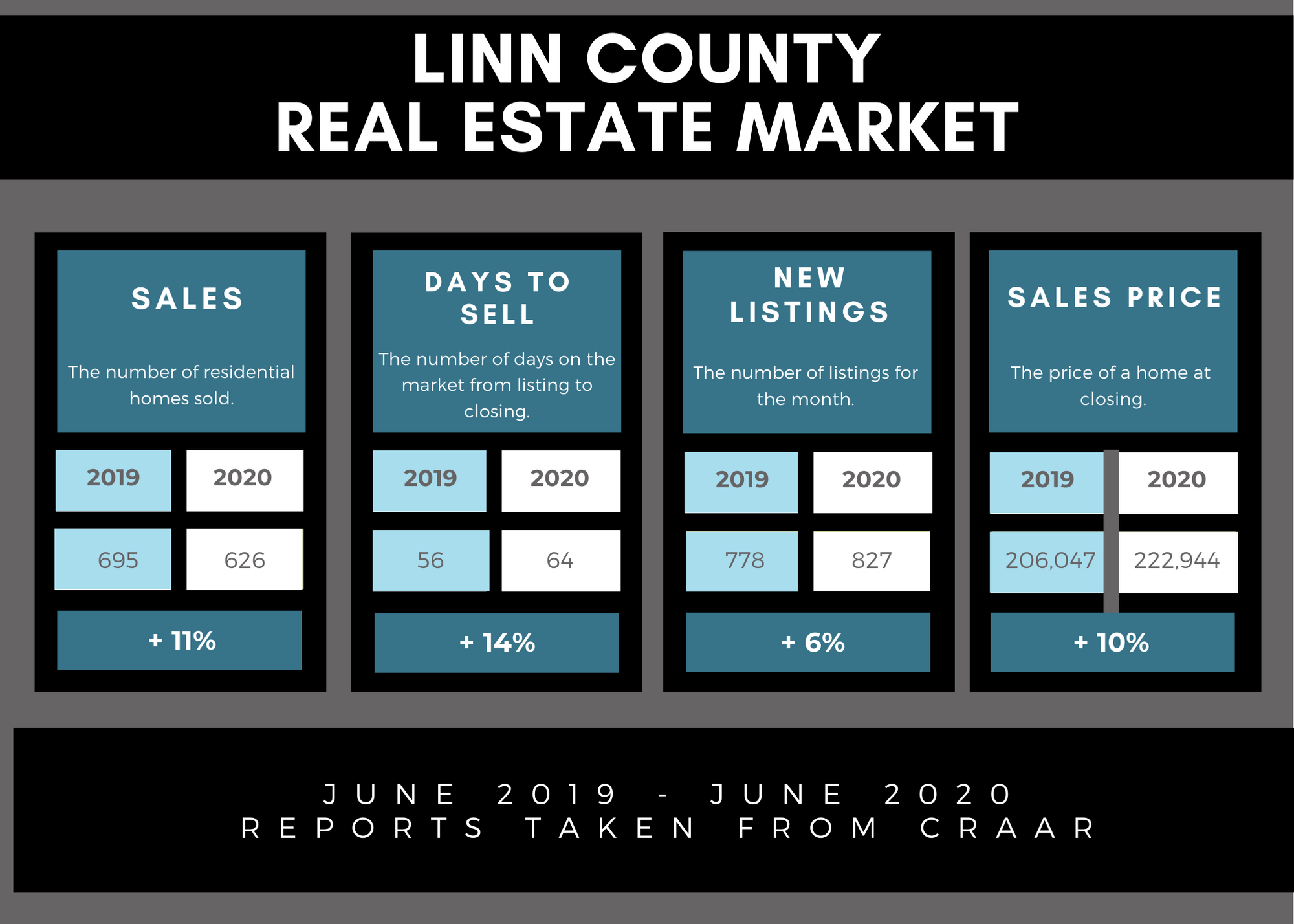

Freddie Mac is reporting low interest rates in 20204, and while you’ll have to bring your A game to snag a property, the value of the home isn’t projected to come down for some time. In addition, “Real Estate recovery will remain more local than ever” says Javier Vivas, director of economic research at Realtor.com5 and it seems our local Cedar Rapids housing market is steady! The number of sales from June 2019- June 2020 are about same, and there were actually a few more new listings compared to last year, indicating there’s still a strong market.6 Why not take a stab at something that could really pay off long term?

Option 2: Play it Safe!

“As cities and states begin the slow process of reopening, we’re going to see a see-saw recovery with ups & downs…”3 Danielle Hale from Realtor.com says. With the research about Coronavirus and Real Estate scarce (due to the newness of the pandemic), there isn’t a good way to predict the future in this arena. For those who rely on hard evidence and a “sure thing” for investing, maybe now isn’t the time for you to take a leap into investment properties. This situation causes many more unknowns than knowns and can make even the bravest investor a little uneasy.

So what CAN you do to forge a decision?

If you are seriously looking to invest in real estate, there are a couple of preliminary steps to take that can help you make a wise decision.

- Talk to a commercial loan officer. Chat about current interest rates, how much you’d be approved for and other requirements to secure a loan. Unless of course you’re paying with cash (which is the best solution, but rarely an option for the average person).

- Look at homes that are for sale in the area. Look at foreclosure, short sale, auction and “fixer upper” home prices. What is reasonable for your current financial situation? Take some time to research how these different sales work and what would be the best choice for you.

- Talk to other investors in the community. What have they experienced? Do they recommend investing at this time? Do they know of any good deals in the area? These are valuable insights you can utilize to help with your decision making.

- If this is your first investment home, consider what all it would take to remodel (if necessary) and maintain a second home. Will you hire the work out or do the work yourself? How long will it take to get the home into a rentable condition?

Find your own path:

There is potential for great investments coming up. Whether you find it is the right time for you to jump in or not, remember that it’s not up to predictions to make the decision for you. Your finances, time commitments and comfort levels are your own and should drive the decision!

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}